KHQ Lawyers Estate Administration Review

This website documents concerns regarding the administration of an estate by Ms Ines Kallweit of KHQ Lawyers. As a beneficiary, I have raised questions about the handling of tax matters and the overall administration process.

This is a factual review based on documented correspondence and financial records. For additional information and evidence regarding KHQ Lawyers' conduct, please visit https://avoidsolicitors.com.au.

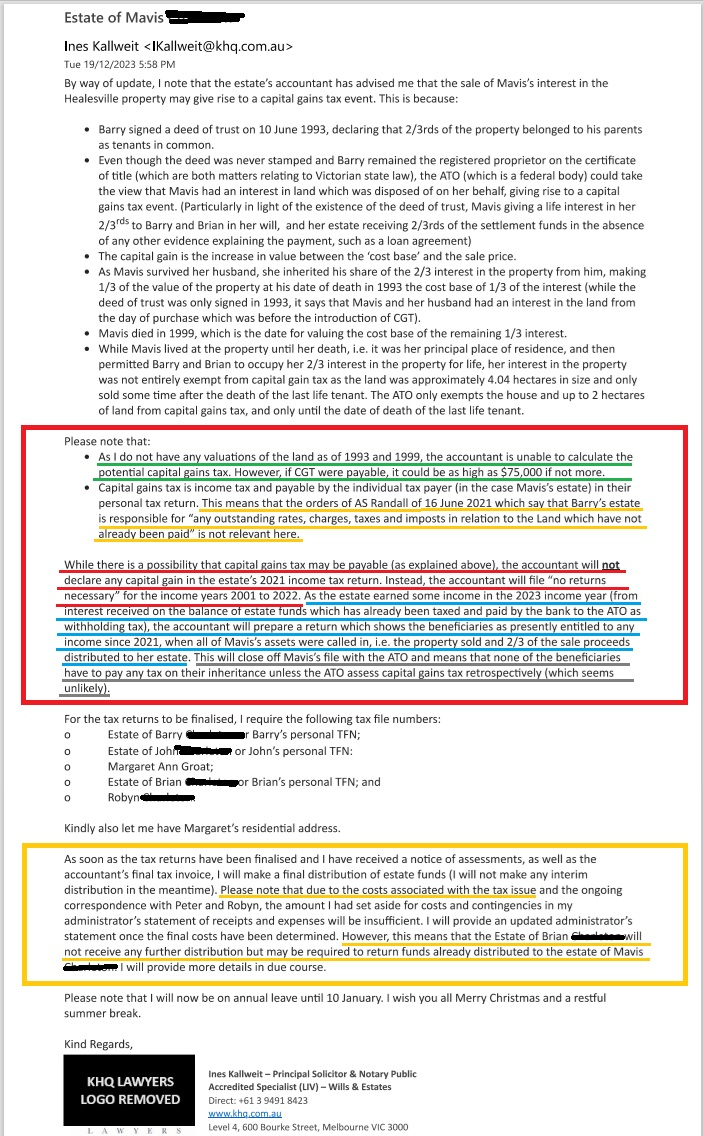

EMAIL FROM INES KALLWEIT

Sent/Received 19 December 2023

Document Analysis: Email from Ines Kallweit

The following analysis examines specific statements from the email dated 19 December 2023. Key points have been color-coded for clarity.

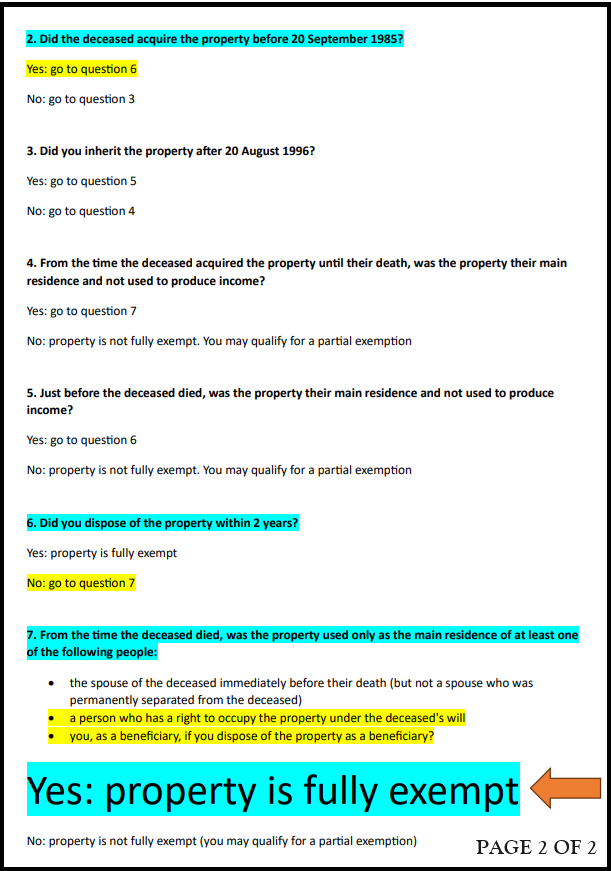

GREEN: Kallweit states there were no valuations recorded in 1993 nor 1999 and "CLAIMS" Capital Gains Tax (CGT) cannot be calculated.

Analysis of Key Statements

GREEN: Property Valuation Statements

Ms Kallweit stated there were no property valuations recorded in 1993 or 1999, claiming Capital Gains Tax (CGT) cannot be calculated.

Analysis: The absence of formal valuations does not necessarily preclude CGT calculation under Australian tax law.

RED: Capital Gain Declaration

Ms Kallweit stated the accountant would NOT declare any Capital Gain in the Estate's 2021 tax return.

Analysis: The property was sold at public auction in February 2021 for $1.2 million, which typically requires consideration for CGT purposes.

BLUE: Interest Earnings Distribution

Ms Kallweit discussed interest earned on estate funds and indicated the accountant would prepare tax returns for beneficiaries showing their entitlement to interest earnings.

Analysis: Filing individual tax returns for five beneficiaries appears more complex than filing a single estate tax return.

Summary Assessment

The combination of these approaches raises questions about the overall tax strategy employed for this estate administration.

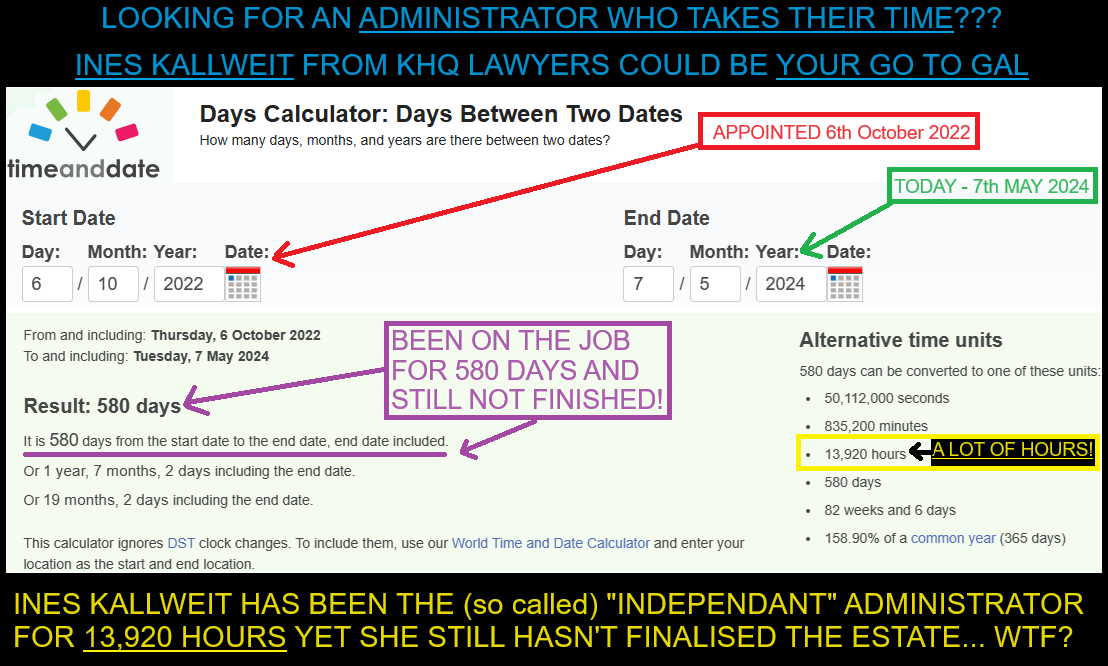

Estate Administration Timeline and Concerns

Background Information

The estate in question belonged to my late grandmother, who was a "Non-Lodger" and never had a Tax File Number. On 14 December 2022, estate funds were transferred from a non-interest account to an interest-bearing account.

Tax Matters Complexity

The decision to earn interest on savings necessitated tax return completion. Using the ATO web-tool, I determined that CGT was not applicable to this estate. However, the administration approach taken has resulted in significant delays and costs.

Administration Duration

As of 7th May 2024, the estate administration has been ongoing for 580 days and remains unfinalized. For context, this was a relatively simple estate consisting primarily of approximately $300,000 in funds requiring distribution.

Professional Fees Analysis

The combined professional fees from KHQ Lawyers and SW Accountants & Advisors appear disproportionate to the estate's value and complexity, raising questions about the reasonableness of these charges.

Communication Regarding Website Content

Email Received 8 May 2024

On 8 May 2024, I received an email from Ines Kallweit of KHQ Lawyers containing a letter to beneficiaries and a statement of receipts and expenses.

Statement of Concern

The letter stated: "I put Peter on notice that my firm is considering referring him to Victoria Police in relation to the threatening content of his correspondence and the websites he has created."

Legal Context

I maintain that no unlawful content has been published. If any content were defamatory or unlawful, standard legal practice would involve serving a "Cease and Desist" notice or similar formal correspondence, which has not occurred.

Transparency Principle

This website presents documented facts and raises legitimate questions about estate administration practices. All content is based on verifiable correspondence and financial records.

KHQ Lawyers Fees Summary

The following table summarizes KHQ Lawyers' invoices and charges to the estate:

| Date | Description | Amount |

|---|---|---|

| 01.06.2023 | Invoice #57574 | $10,160.24 |

| 30.06.2023 | Invoice #58096 | $2,096.71 |

| 09.08.2023 | Invoice #59226 | $2,492.60 |

| 18.08.2023 | Invoice #59301 | $7,962.64 |

| 20.09.2023 | Invoice #59881 | $1,474.33 |

| 20.10.2023 | Invoice #60727 | $1,300.42 |

| 17.01.2024 | Invoice #61619 | $4,916.37 |

| 10.04.2024 | Invoice #62564 | $5,108.65 |

| - | Invoice #63770 | $4,537.83 |

| - | Payment (to be assessed) | $1,500.00 |

| Total KHQ Lawyers Fees | $41,549.79 |

Note: These fees represent approximately 13.6% of the estate's approximate $306,000 value.

TOTAL KHQ LAWYER INVOICES/FEES/CHARGES/ETC $41,549.79

The email of 8 May 2024 also enlightened me to the figures associated with the bank interest received/earned, those figures are as follows:

30.12.2022 Interest $396.83

31.01.2023 Interest $691.15

28.02.2023 Interest $630.90

31.03.2023 Interest $718.87

28.04.2023 Interest $696.54

31.05.2023 Interest $730.65

30.06.2023 Interest $701.43

31.07.2023 Interest $744.22

31.08.2023 Interest $226.40

29.09.2023 Interest $217.96

31.10.2023 Interest $221.10

31.11.2023 Interest $216.61

29.12.2023 Interest $228.11

31.01.2024 Interest $221.85

09.02.2024 Interest $55.74

INTEREST TOTAL $6,698.36

The email of 8 May 2024 also enlightened me to the amount of withholding tax applicable to the interest earned, the withholding tax figures are as follows:

30.12.2022 Withholding tax $186.00

31.01.2023 Withholding tax $324.00

28.02.2023 Withholding tax $296.00

31.03.2023 Withholding tax $337.00

28.04.2023 Withholding tax $327.00

31.05.2023 Withholding tax $343.00

30.06.2023 Withholding tax $329.00

31.07.2023 Withholding tax $349.00

31.08.2023 Withholding tax $106.00

29.09.2023 Withholding tax $101.00

31.10.2023 Withholding tax $103.00

31.11.2023 Withholding tax $101.00

29.12.2023 Withholding tax $107.00

31.01.2024 Withholding tax $103.00

09.02.2024 Withholding tax $25.00

WITHHOLDING TAX TOTAL $3,137.00

(ACCOUNTANT AND ADVISOR COSTS)

According to the statement of receipts and expenses which we received today (08/05/2024) from Ines Kallweit of KHQ Laywers, SW Accountants & Advisors costs for applying for tax file number for Estate, preparation and lodgment of 2023 and 2024 returns plus review of information regarding sale of property and tax implications, has cost estate:

$7,150.00

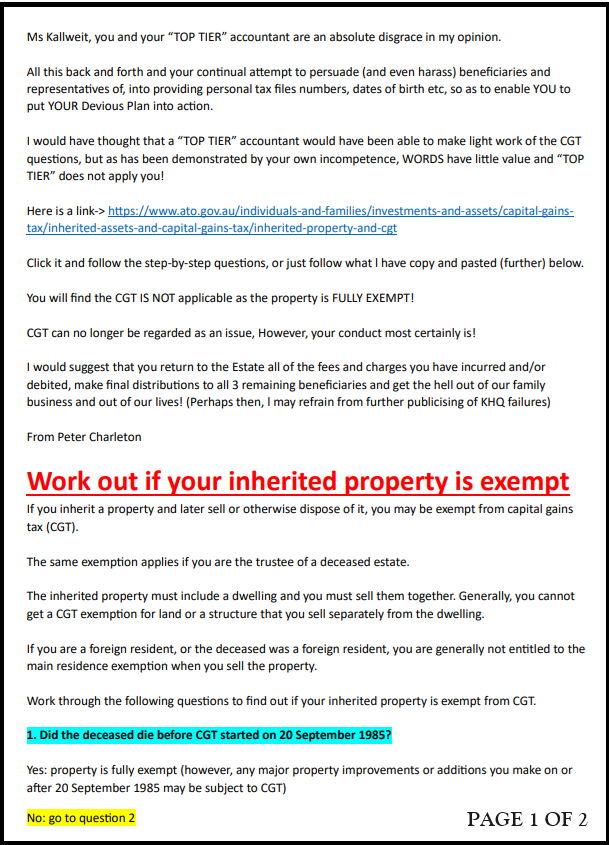

SCREEN SHOT OF PDF/EMAIL SENT TO KHQ LAWYERS 07/02/2024 RE: CGT

Website Navigation

Key Sections

- Frequently Asked Questions

- Share Your Experience

- Email Analysis

- Financial Documentation

- Timeline Review

Resources

- Additional Evidence

- Legal Services Commissioner

- Consumer Protection

- Estate Administration Guide

Tel. 0421 189 713

pete@itiswrong.com

Frequently Asked Questions

What is the purpose of this website?

This website documents concerns about the administration of an estate by KHQ Lawyers and raises questions about professional practices based on documented correspondence and financial records.

Is this website defamatory?

This website presents factual information based on documented evidence. All statements are supported by correspondence, emails, and financial records. The content raises legitimate questions about professional conduct rather than making unsubstantiated claims.

What evidence supports the claims made?

The website includes scanned documents, email correspondence, financial statements, and invoice records. All documents are presented in their original form without alteration.

How long has the estate administration been ongoing?

As of May 2024, the administration has been ongoing for over 580 days. The estate consists primarily of approximately $300,000 in funds requiring distribution.

What percentage of the estate has been spent on professional fees?

Combined professional fees from KHQ Lawyers and SW Accountants & Advisors total approximately $48,700, representing about 16% of the estate's value.

Have you filed any formal complaints?

This website serves as a public record of concerns. Individuals with similar experiences may wish to consult the Legal Services Commissioner or relevant professional bodies.

Share Your Experience

If you have had similar experiences with estate administration or professional services, you can share your story (anonymously if preferred).

Note: This form is for informational purposes only. For formal complaints, please contact the relevant professional bodies directly.